Blogs

For generations, Indians have cherished the dream of possessing a home of their own. It was part of the commonly portrayed essentials – Roti, Kapda and Makaan. Budget 2019-20 has given a much-needed boost to the affordable housing segment catering to the lower income and the middle-class. This segment has seen renewed activity in recent years, ever since the NDA Government took over reins in New Delhi, with a slew of positive steps including the ground-breaking Pradhan Mantri Awaas Yojana (PMAY), which incentivises housing finance companies that build homes focused on the economically weaker sections (EWS) and low-income groups (LIG). The budget will help revive the sluggish housing sector and help reduce the unsold inventory in the books of builders.

Let us look at the provisions of Budget 2019-20, specifically targeting the real estate sector and home buyers, and how additional money saved could be channelized towards acquiring a house property.

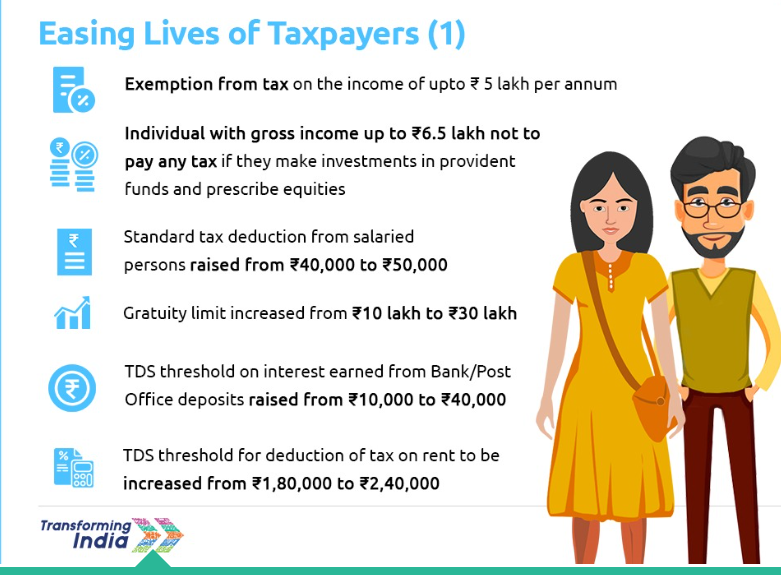

The government announced a full tax rebate on individual income of up to Rs. 5 lakh. Further, if the assessee was to invest in tax saving instruments up to Rs. 1.5 lakh u/s 80C of the Income-tax Act 1961, it translates into a tax–free income of Rs. 6.5 lakh, with the taxable income after deductions being Rs. 5 lakh. Section 80C allows deduction of expenses towards repayment of a home loan and stamp duty, registration charges towards a house property. The rebate under section 87A of Income-tax Act 1961, available since the assessment year 2014-15 has been hiked from Rs. 2500 to Rs. 12,500 per annum. Total taxable income or net taxable income is the income after considering any deductions.

In a nutshell, the Government has put extra money into the pockets of citizens as summarised in the below graphic:

Source: Mygov.in

Scenario 1: Assume in the next fiscal, an assessee has an income of up to Rs. 5 lakh in the financial year. He/she is permitted to claim the entire tax payable as a tax rebate.

Scenario 2: If an assessee is having a gross income of Rs. 6.5 lakh for the financial year 2019-20 and makes an investment of Rs. 1.5 lakh under section 80C her net taxable income comes down to Rs. 5 lakh. Her resultant tax liability would be Rs. 12,500 (5% of Rs. 2.5 lakh) excluding cess (income up to Rs. 2.5 lakh is exempt from tax as per the current income tax slabs). However, as her income is up to Rs. 5 lakh, she is liable to claim a rebate of Rs. 12,500, and thus her net tax payable would be zero. This means that while the assessee is still liable to file returns, the tax payable is zero.

Further, if one was to consider the additional tax benefits u/s 24 towards interest on a home loan, u/s 80D towards medical insurance and u/s 80CCD towards pension contribution, the tax-free income is hiked to Rs. 7.5 lakh. According to an ET survey, these savings are expected to flow into the affordable housing sector where the home loans are usually in the tune of Rs. 10 lakh with EMIs ranging up to Rs. 10,000.

It is important to note the difference between rebate and exemption. Exemption reduces the total taxable income, while rebate reduces the tax outflow (e.g. rebate under Section 87 of the Income Tax Act 1961). The former applies mostly to middle-class individuals with income of Rs. 5 lakh up to Rs. 7.5 lakh, subject to allocating Rs. 1.5- 2.5 lakh in specific investments and thereby reducing the taxable income to Rs. 5 lakh.

The latter applies predominantly to the LIG with income up to Rs. 5 lakh, where there is 100% tax rebate and no investment requirement.

Increase in standard deduction for salaried people including pensioners, from Rs. 40,000 to Rs. 50,000, will result in higher disposable incomes. This results in better home loan EMI repayment capability.

Conclusion: Tax matters aside, this is the best time to invest in a home that fits your bill. A house property is a significant investment with financial implications throughout one's lifetime. With rising inflation and escalating costs, the house purchase decision should not be postponed to later. Budget 2019-20 has ensured several individuals, estimated at 3 crore are financially better off than before. This can be fruitfully channelised towards realising their real estate goals. This also aligns with the Government’s homeownership vision for

India: Sab ka Sapna...Ghar ho Apna.

How HFCs focussed on affordable housing finance for the informal sector are implementing this goal

Read more